Before you file, see what your tax bill is really costing you and how to fix it.

In 3 days, I'll show you exactly what your 2025 return is costing you, which strategies in the tax code apply to your income, and we'll build your 2026 plan together so this is the last year your money disappears without you knowing where it went.

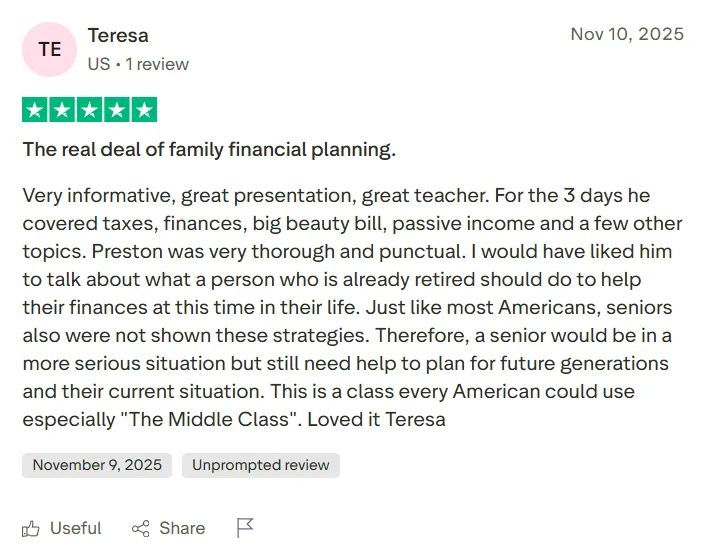

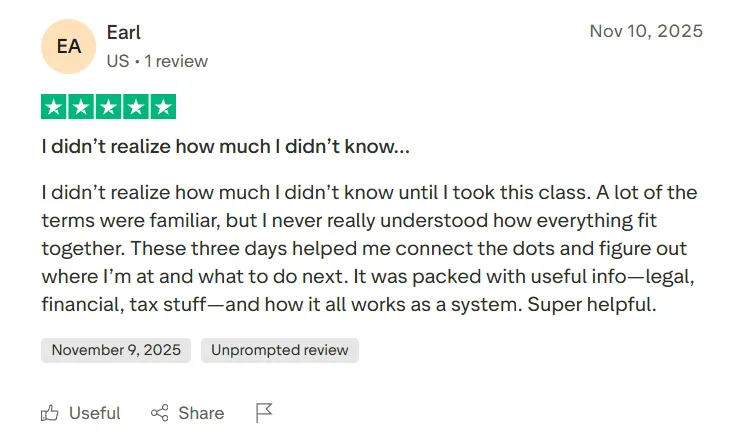

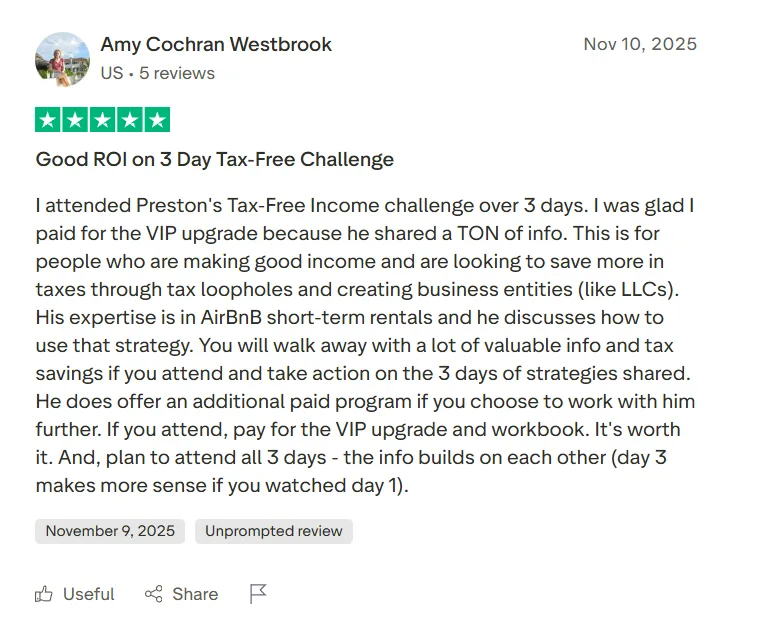

Here's what people who attended the last 3-day challenge said about it.

What You'll Learn In The 3 Days

Day 1Friday, March 27

10 AM-4 PM EST | 6 Hours

Read Your Return: Find Out Where Your Money Is Actually Going

You've never actually read your tax return. Not really. Most people look at one number, sign it, and move on. But every other line on that return is telling you where your money went and why it's not coming back. Day 1 is about seeing the full picture for the first time.

You'll Learn

The middle-class money trap: why every raise comes with a bigger tax bill and why earning more can still leave you with less.

Why your 401(k) may be bleeding money through fees, limits, and a tax bill waiting for you later.

How to eliminate high-interest debt and access $50K-$100K in 0% business funding without touching personal credit.

An entity structure deep dive with a guest speaker who has helped tens of thousands of businesses get set up the right way and oversee hundreds of millions of dollars in structures and filings.

You leave with: A clear picture of where every dollar is going, which leaks are costing you the most, and the exact order to fix them.

Day 2Saturday, March 28

10 AM-4 PM EST | 6 Hours

Build Your Strategy: The Exact Playbook To Keep $20K-$50K More Every Year

Now that you know where the leaks are, Day 2 is where we build the plan that fixes them. This is the day that changes your financial life.

You'll Learn

The W-2 taxes playbook: how people making $1M+ pay less in taxes than someone at $80K, and which strategies apply to your income.

The investor playbook: how to build wealth in accounts that never get taxed, including Roth conversions, backdoor strategies, and legal ways to offset gains.

How to start a tax-advantaged Airbnb business without buying property or quitting your job, with the potential to create $5K-$15K a month.

The complete wealth acceleration system: how the strategies stack together and in what order so they actually work.

You leave with: Every strategy that applies to your income identified, valued in real dollars, and prioritized. You'll know exactly what to implement first, second, and third.

Day 3Sunday, March 29

10 AM-4 PM EST | 6 Hours

Lock Your Plan: Walk Away With A Dated, Dollar-Valued 12-Month Roadmap

A strategy that stays in your head is not a plan. It's a wish. Day 3 is about turning everything from the first two days into a document you can execute on starting Monday morning.

You'll Learn

Advanced tax optimization with a guest speaker who has worked with complex structures across a huge number of businesses and large amounts of assets: trusts, family planning, and how to protect what you build.

Your 12-month implementation roadmap: month 1, month 2, month 3, all the way through the year, with the moves dated and tied to dollars.

Real case studies from working professionals who implemented these strategies, so you can see what this looks like at your income level.

You leave with: A completed, dated, dollar-valued 12-month plan. When you file on April 15, you'll know exactly what you're doing differently for 2026. That's the last time your return looks like this.

VIP also gets the asset protection masterclass, plus live roundtable Q&A on Day 2 and Day 3.That is where Preston breaks down the LLC, S-Corp, trust, and holding company structure behind his own portfolio.

You are not starting from zero. You've read the books, heard the podcasts, maybe even talked to advisors and CPAs. The problem is not a lack of information. The problem is that none of it has turned into a clear plan.

✕

Every raise comes with a bigger tax bill. You work more, earn more, and still feel behind.

✕

Big financial goals keep getting pushed back because you never know which move should come first.

✕

Every money decision feels like a coin flip. Pay off debt or invest? Max out the 401(k) or save for the next opportunity?

✕

You keep hearing smart ideas, but none of them connect into a plan you trust enough to execute.

This challenge helps you connect the dots. You'll see the leaks, pick the moves that fit your life, and leave with the order to work through them.

💭"Think like a millionaire"

📊"Assets vs. Liabilities"

💰"Make your money work"

📚"Read Rich Dad Poor Dad"

☕"Cut your daily coffee"

🏃"Quit your job"

The Patterns That Keep Repeating

If these feel familiar, that's the point. The problem usually is not effort. It's that the same broken money pattern keeps replaying every year.

You keep paying more taxes every year.

Every raise, every promotion, every side hustle dollar pushes you into a higher bracket. You're earning more and keeping less. And nobody around you can explain why.

Your CPA files your return but never calls you with a plan.

They're good at what they do. But when's the last time they called you in June and said you had $40,000 exposed and showed you how to keep it? That call never comes.

You've Googled it, watched YouTube videos, and saved reels. And you still haven't made a move.

S-Corp. LLC. Solo 401(k). Cost segregation. You know bits and pieces. But you still do not know what fits your income, what comes first, or what any of it is worth. So nothing changes.

You keep saying "next year."

Next year I'll set up the LLC. Next year I'll look into real estate. Next year I'll figure out the tax side. Then next year comes and you file the same return with the same pit in your stomach.

The Problem Isn't Your Income. The Problem Is That Your Money Is Structured Wrong.

The way your paycheck flows from your employer to your bank account to the IRS was set up once, years ago, and never touched again. Smart people stay stuck because the money is moving through a system that was never designed to help them keep more of it.

And every year you don't fix it, the gap gets wider.

The W-4, the 401(k) percentage, the debt decisions, the side income, the tax return, the entity structure. None of the pieces are talking to each other. That's the real problem.

Why Most High Earners Stay Stuck

What breaks is the model. The default playbook was written for average earners, the planning starts too late, and nobody in your financial life is paid to orchestrate the whole thing.

Broken Model #1

You're following rules designed for people who make $50K.

Max out the 401(k). Build a 6-month emergency fund. Pay off your mortgage early. At $150K+, the math changes. The strategies change. The tax code treats you differently.

Broken Model #2

Your tax strategy is "file and hope."

You earn money all year, then hand everything to your CPA in April and hope the number isn't too bad. The people who pay the least in taxes planned in January for December.

Broken Model #3

Nobody connects the dots for you.

You have a CPA who files, an advisor who sells products, and a bank that holds your money. None of them talk to each other, and none of them are paid to save you money.

Broken Model #4

There is no one in your financial life whose job is to make all the pieces work together.

That's what this event does. It gives you the structure, the order, and the real numbers so you stop guessing.

The Tax Code Changed. Your Return Hasn't Caught Up Yet.

Last July, the government passed the biggest tax code rewrite since 2017. Fifteen provisions changed. Some are permanent. Some expire in four years. Some are retroactive to 2025, which means they affect the return you're about to file right now.

Your CPA updated the software. The brackets are correct. But did anyone sit down with you and show you which of these changes actually apply to your income, which ones you should act on now, and which ones you lose if you wait?

This is the first year you're filing under the new law. And for several of these provisions, the clock is already ticking. Before You File is built around this exact moment and what to do before April 15.

Step 1

Keep More Of Your Current Income

You look at legal tax strategies first so more money stays in your control before you try to build anything new.

Step 2

Free Up Monthly Cash Flow

High-interest debt and bad financial structure get cleaned up so your household has breathing room again.

Step 3

Redirect Cash Into Better Vehicles

You stop defaulting to average-person retirement advice and start evaluating cash-flow, tax-advantaged, and business-based options more clearly.

Step 4

Protect And Scale The Plan

Entity structure, protection, and order of execution keep the plan durable. This is where wealth starts to feel real instead of theoretical.

If this already feels different, that's the point.

Get In The Room And Build The Plan While It's Fresh

You do not need more scattered information. You need the sequence, the numbers, and the live walkthrough before you file again on autopilot.

Here are a few of the returns we sat down with and what we found once we looked at the full picture. One of these will probably feel close to your situation.

Lauren

$125K/year

Year 1 Value$61K - $109K

She was losing $1,237 every single month to a W-4 she filled out in 2019. That's $14,840 a year, gone before she ever saw it.

Her plan identified 6 strategies she qualified for but wasn't using. The STR strategy alone created more tax savings than most people's entire annual 401(k) contribution.

Chad

$180K combined

Year 1 Value$18.5K - $43.5K

His CPA does a good job and never misses a deadline. But there's a gap between filing and optimizing.

Chad's plan mapped 8 strategies to his income. Each one had a dollar value, an implementation week, and the exact documentation required.

Michelle & Trenton

$300K combined

Year 1 Value$86K - $192K

At a 46% combined bracket in San Francisco, every dollar of deductions saves 46 cents. That math changes everything.

Their plan identified 8 strategies totaling $86K-$192K in year-one value, plus the right structure for family planning and long-term protection.

Daniel

$250K/year

Year 1 Value$55.9K - $68.3K

He'd researched for years. He knew the strategies. He didn't need more information. He needed a sequence.

Do this Monday. Do this Wednesday. Apply here Thursday. Wait 14 days. Then do this next. The order matters more than the strategies.

Elizabeth

$150K/year

Year 1 Value$28K - $62K

She was paying $43,000 a year in taxes. After restructuring: $28,500. That's $14,500 back every year.

What made her plan different: she had almost no capital. She needed strategies that cost nothing to implement. The first 5 moves cost $0.

Who This Is For, And Who Should Skip It

This event works best when you already have income, already know something is off, and are ready to finally turn that awareness into a plan.

Who This Is For

You make roughly $100K-$500K and know there is real money leaking out of your current setup.

You have a CPA, advisor, or existing financial setup, but nobody is actually mapping your next moves in order.

You have heard about LLCs, S-Corps, Roth conversions, STRs, or tax strategies but do not know which ones actually fit you.

You are tired of filing the same kind of return every year and promising yourself you'll deal with it later.

You want a plan with dollar values, tradeoffs, and sequence, not another generic money pep talk.

You have a spouse or partner and you want to finally get on the same page about money.

You are willing to implement, ask questions, and make decisions once the right path is clear.

Who This Is Not For

You want a loophole, a magic trick, or a get-rich-quick pitch. This is implementation, not hype.

You make under about $75K and need beginner budgeting help more than strategy coordination.

You want somebody to do everything for you without you making any changes or decisions.

You are looking for a passive webinar to half-watch while changing nothing afterward.

You want broad theory without being challenged to pick an actual sequence and act on it.

"I've Heard This Before."

Fair. Here's why this is different.

Most financial content gives you information. This gives you a plan.

Not "here are 10 tax strategies." Here is your plan, matched to your income, with dollar values attached, in the order you should implement it.

Most events are taught by people who teach events.

Preston built a $20M+ portfolio, has saved over $500K in taxes personally, got audited after a $500K year and held up clean, and has had 4,400+ people go through this system.

Most advice assumes you have the same situation as everyone else.

This event covers 40+ strategies across multiple income levels. If you make $150K with a side business, your plan should not look like someone making $300K W-2 only.

This is live. You can ask questions. And the guarantee removes your risk.

VIP members get live roundtable Q&A on Days 2 and 3. If you show up to all 3 days, take notes, ask questions, and still do not leave with clarity on what to do next, email within 7 days for a full refund.

If you're still reading, you probably already know this is your problem.

Don't Wait Until After You File To Wish You Had A Plan

Get the live breakdown, the sequence, and the implementation order now, while there is still time to change what happens next.

You Don't Have To Trust Us. You Can Check Right Now.

Here are 3 things you can verify before spending a dollar.

If you're W-2

Pull up your most recent paystub. Find your federal withholding. Multiply it by your pay periods. Compare that to your actual tax bill from last year. If there's a gap, that's cash flow you're handing the IRS every paycheck.

If you have business or 1099 income

If you're still a sole proprietor paying self-employment tax on all your profit, you may already be paying thousands more than you need to. For many people, the gap is $4,000-$10,000 or more a year.

If you have business expenses you don't track

Home office. Vehicle mileage. Phone. Internet. Equipment. Most people leave $2,000-$6,000 on the table simply because they don't track correctly or don't know what documentation matters.

That's before the rest of the plan

If even one of those applies to you, you may have already found enough value to pay for this event many times over. And those are only a few of the moves covered in Before You File.

General Admission vs VIP

Choose the level of access that fits how much support and implementation depth you want before April 15.

General Admission

$97$47

You'll walk away with a complete action plan.

The middle-class money trap breakdown and your escape plan

401(k) alternatives that actually build wealth faster

Tax strategies that save high earners $20K-$50K annually

Debt elimination and access to $50K-$100K in funding

Pre-challenge $15M Asset Protection Masterclass with Preston

—

✓

Live roundtable with Preston (Days 2 & 3)

—

✓

Ask Preston questions directly

—

✓

15+ hours of lifetime replay access

—

✓

All slides, notes & materials

—

✓

Guarantee

Show Up, Learn, Ask Questions. If It Misses, Ask For Your Money Back.

Go through the challenge. Take notes. Build the plan. If you do not leave with more clarity on what to do next, email within 7 days and the ticket is refundable.

Schedule

March 27-29, 2026

Day 1Friday, March 27 | 10 AM-4 PM EST

Day 2Saturday, March 28 | 10 AM-4 PM EST

Day 3Sunday, March 29 | 10 AM-4 PM EST

VIP also gets the pre-challenge masterclass before the event starts, plus live roundtable calls on Day 2 and Day 3.

How I Learned This The Hard Way

I watched my parents work nonstop and still almost lose everything.

This is not theory for me. It came out of watching my family work hard, almost lose everything, and then spending years trying to break that same cycle in my own life.

What I Saw Growing Up

My parents were immigrants. They came to the U.S. with nothing. They worked 12 to 16 hours a day, 7 days a week, and still almost lost everything following the same script most people still follow now.

They believed hard work was the answer. More hours. Save what's left. Play it safe. They did everything right according to that script and still ended up close to foreclosure.

I was in middle school when someone from the foreclosure office showed up at our house. My parents never told us how bad it had gotten. That stuck with me.

Preston's father coming to the U.S. in 1985.The grind that shaped our family.Grandma raising us while my parents worked.

The Loop I Fell Into

By my 20s, I was following the same script. I tried random businesses. They failed. So I went corporate and thought that was the responsible move.

On my first day at my corporate job, I remember thinking: I have to do this for the next 40 years? I knew right away this wasn't it. I just didn't know how to get out.

Then I got married. Right after the wedding, I checked our bank account. We had $685 left. I had spent everything on the ring and the honeymoon. Bridget and I moved into my parents' basement for eight months.

She was working long shifts as a respiratory therapist. I was grinding through quotas. We barely saw each other. One job. One stream of income. The IRS taking 30-40%. No structure. No protection. No plan.

$685 left after the wedding.The basement room we moved into.

What Changed

Then we had our first son. I was in the hospital, holding him, while my phone kept buzzing. Emails. Notifications. Work. I remember reaching for my laptop and thinking, if I stop for a day, does everything fall apart?

That was the moment something broke. I started researching every night. That led me to investing. Investing led me to really looking at my tax bill. What I saw made me angry. The system was built this way and nobody was teaching people like us how it actually worked.

We started fixing the leaks. Building new income streams. Learning how to separate what we earn from how it gets taxed. The first real win was a cost segregation study that saved us tens of thousands in taxes. That proved this was real.

Then we started stacking strategies the right way. Used leverage the right way. Built income that didn't depend on us showing up every morning. That's how we broke the loop.

The hospital moment that changed everything.

Why This Event Exists

Today Bridget and I have built a $20M+ portfolio. I became financially independent at 28. I'm still actively building and still using the same strategies I teach in this event.

The year I made $500K, the IRS sent me a $46 refund. They audited me after that. Everything held up because none of this is a loophole. Every strategy has a section number in the tax code.

I retired my parents and bought them a rental property that covers their retirement. When I told my mom she never had to work another day, she broke down.

That's why I'm hosting Before You File. April 15 is coming and most people are about to file a return that costs them far more than it should. I want this to be the event that changes that for you and your family.

$20M+Portfolio built from scratch

6M+People reached with money education

28Age Preston became financially free

1 PlanTax, debt, cash flow, protection, all tied together

What People Say After Going Through This

Not vague motivation. Real people, real starting points, and concrete outcomes they were able to tie back to the plan.

Case Study | Corporate sales to investor

Dustin Cotten

"I didn't want to work my whole life just to be told I couldn't use my own money."

Dustin was in corporate sales, looking for a way out. The turning point came when his girlfriend's mom passed away at 62 with savings locked up. He decided he was done building a life he couldn't actually use.

🏠

First property in 30 days, $3K/month

📈

7 properties in under 2 years

💰

$56K net profit in one month

✅

Walked away from his 9 to 5

Case Study | High-income earner fixing tax drag

Galin

Turning Taxes Into Cash Flow and Long-Term Growth

Before, Galin was working hard but watching too much disappear to taxes and overhead. The plan helped him turn that lost money into actual investment capacity and long-term growth.

🏦

$100K+ in tax savings and paper losses

📈

Six figures redirected into long-term investments

Estimated 12-Month ROI~$150,000+

Case Study | W-2 household building early freedom

Abigail

Eliminating Taxes And Building Early Freedom

Before, their household was stuck watching too much of a W-2 paycheck disappear to the IRS. After putting the right pieces in place, they had a path to legally cut taxes, create earlier income access, and move money into assets that actually compound.

🏦

~$52,500 cash refund from tax savings

🧾

$30K shifted into 0% tax brackets

🏠

Six-figure savings sheltered through new structures

📈

$50K-$100K estimated 12-month ROI

March 27-29, 2026 | Live on Zoom

This Gets Expensive To Put Off.

One more year of overpaying taxes, carrying bad debt, and making disconnected money decisions costs more than the ticket. Get the plan, build the roadmap, and decide from clarity instead of stress.